Mihir Das, MFA-P, IFIC

- ADVISORY MONEY STRATEGIES INC

- 5580 Explorer Dr, Suite 502, Mississauga, ON L4W 4Y1

- Telephone: 437-214-7224

- Email: mihir@amstrategies.ca

- Web: https://amstrategies.ca

Mihir Das is helping families and small businesses in the Ontario Region, particularly in the Greater Toronto Area. He works with you one-on-one to provide guidance and unique planning solutions on topics such as Income Protection, Cash Flow Management, Retirement, and Estate Planning. Mihir cares about building long-term relationships and getting to know you and/or your company in-depth so he can offer you the best advice possible to fit your needs. He aims to help clients reach their greatest potential and to make a meaningful difference in their lives. Get In touch with Mihir Das. He would love to hear where you are in your journey and how he can help.

About Me

Mihir started as a financial advisor at Sun Life Financial. After one and a half years, he joined Advisory Money Strategies Inc. as an Advisor and Vice President, Sales.

Mihir mostly work with families, professionals, and business owners. The clients’ needs, goals, and financial well-being are always first and foremost. He help attain their best interests by creating a financial plan to meet their changing needs throughout their lifetime. He build long-term relationships based on trust, integrity, and transparency, integral in ensuring the success of my client’s goals and dreams.

Mihir has volunteered for over fifteen years with various community and cultural organizations. His hobbies and interests are painting, travel, and various cultural activities, especially drama and acting.

He is an independent professional advisor, working with Advisory Money Strategies Inc., He works with most of the renowned insurance companies.

Mihir mostly work with families, professionals, and business owners. The clients’ needs, goals, and financial well-being are always first and foremost. He help attain their best interests by creating a financial plan to meet their changing needs throughout their lifetime. He build long-term relationships based on trust, integrity, and transparency, integral in ensuring the success of my client’s goals and dreams.

Mihir has volunteered for over fifteen years with various community and cultural organizations. His hobbies and interests are painting, travel, and various cultural activities, especially drama and acting.

He is an independent professional advisor, working with Advisory Money Strategies Inc., He works with most of the renowned insurance companies.

My Process

Here are the key elements I follow :

- - Canadian Anti-Spam Laws (C.A.S.L): I embrace the anti-spam laws in communication.

- - Generic Life Insurance Needs Analysis: This process determines how my coverage insured person needed.

- - Engagement Letter: An engagement letter setting out the scope and the purpose of our work together. The client and Agent (myself) both sign this document.

- - Advisor Disclosure: I provide full disclosure of whom I deal with, how I get paid, and what services are provided.

- - Errors and Omissions Insurance (E&O – Professional Liability Insurance): Designated professional advisors are fully covered by E&O insurance.

Services

Personal Life Insurance

![]() Life insurance is one of the most important ways you can protect your loved ones financial future. Life insurance provides whomever you choose with a one-time, tax-free payment when you die, as long as you continue to pay your premiums or paid-up premium.

There are different types of life insurance and different ways to make it work for you. It’s not only to protect your family. It can also be part of your financial plan, so you may be able to access money in your policy while you’re alive.

There are 2 basic types of life insurance coverage: Term, Permanent and Universal Life. Each has unique features designed to meet different needs.

Life insurance is one of the most important ways you can protect your loved ones financial future. Life insurance provides whomever you choose with a one-time, tax-free payment when you die, as long as you continue to pay your premiums or paid-up premium.

There are different types of life insurance and different ways to make it work for you. It’s not only to protect your family. It can also be part of your financial plan, so you may be able to access money in your policy while you’re alive.

There are 2 basic types of life insurance coverage: Term, Permanent and Universal Life. Each has unique features designed to meet different needs.

- Term insurance: Features included temporary coverage, lower cost, fixed payments, option to convert to permanent.

- Permanent insurance: Features included lifetime coverage, higher cost, flexible payments, opportunity to build cash value.

- Universal Life insurance: It’s a form of permanent life insurance with an investment savings element plus premiums and a death benefit that are flexible.

Corporate Owned Life Insurance

Life insurance has long been used as a financial and estate planning tool for business owners. Whether it’s help to cover a tax liability at death, to ensure adequate funding for a shareholders’ agreement, or to put a capitalization program in place for a shareholder’s policy, a life insurance policy will often be purchased by a corporation or a group of corporations, or even a trust. In certain situations, there are specific rules around choosing the owner, premium payor and beneficiary of the policy that must be followed to avoid unexpected – and undesired – tax and legal repercussions. With that in mind, the purpose of this document is to outline how life insurance can be used as a financial and estate planning tool for business owners. Why corporate-owned life insurance? Several business reasons might justify corporate ownership of a life insurance policy. Generally, corporate ownership of insurance will, if the applicable rules are followed, produce definite advantages from a financial, tax, and legal perspective. These advantages, which we’ll look at in more detail later in this document, include the ability to utilize the Capital Dividend Account (CDA), protection for the policy against creditors, streamlined policy management, a more equitable sharing of premium payments, and reduction of the tax cost of the premium. Shared ownership works when two or more parties agree to share a single asset. This way, each party pays only for the benefits they want. Shared ownership using critical illness insurance allows a business to protect itself against financial hardship should a key employee be diagnosed with and survive a covered critical illness. The strategy also provides the employee with an opportunity to participate in the benefits of a critical illness insurance policy. This comprehensive set of tools will help you understand, illustrate and present this strategy. Who to consider: Need for corporate-owned CI insurance, Key person protection, Fund buy-sell agreement, Key employee or owner-manager.

Health Insurance

Critical illness insurance:![]() Critical illness insurance usually covers a one-time lump-sum payment if you're diagnosed with a critical illness. The payment may cover expenses such as daycare or paying bills to make your life more comfortable.

Critical illnesses may include lots of diseases including Cancer, Alzheimer’s disease, Heart attack, Stroke.

Critical illness insurance usually covers a one-time lump-sum payment if you're diagnosed with a critical illness. The payment may cover expenses such as daycare or paying bills to make your life more comfortable.

Critical illnesses may include lots of diseases including Cancer, Alzheimer’s disease, Heart attack, Stroke.

Disability insurance: Disability insurance helps protect you and your family from an unexpected illness or accident. It provides protection if you’re unable to work and earn an income. It can give you a tax-free monthly payment to help replace your income and cover your expenses if an illness or injury keeps you from working. Generally, disability insurance replaces between 60% and 85% of your income. While a disability can often be visible to the naked eye, not all disabilities are so easily recognized. Chronic pain or a mental health issue can also qualify as a disability. Many employers offer disability insurance. However, disability insurance plans are also available through a life and health insurance agent. If you're self-employed, you may want to consider getting disability insurance. It will cover many of your business expenses if you're unable to work. Each disability plan is different. When buying disability insurance, make sure you understand the terms and conditions of the plan. Ask about anything you don't understand.

CPP Philanthropy: ![]() Canadians are looking for ways to reduce that tax burden and instead provide tax efficient funds to their favorite charities. With very few exceptions, every working Canadian over the age of 18 must contribute to the Canada Pension Plan (“CPP”). For many retired Canadians, CPP and Old Age Security benefits (of about $1,100 a month) are vitally important to pay bills and other living expenses. Wealthy Canadians, in contrast, don’t need those benefits to cover their expenses as they just get invested, taxed, reinvested and taxed again. We call that “never spend money”.

Using the CPP Philanthropy™ strategy, their government-supplied benefits can fund the premiums on a significant life insurance policy for the benefit of favoured charities and to enhance estate values.

Canadians are looking for ways to reduce that tax burden and instead provide tax efficient funds to their favorite charities. With very few exceptions, every working Canadian over the age of 18 must contribute to the Canada Pension Plan (“CPP”). For many retired Canadians, CPP and Old Age Security benefits (of about $1,100 a month) are vitally important to pay bills and other living expenses. Wealthy Canadians, in contrast, don’t need those benefits to cover their expenses as they just get invested, taxed, reinvested and taxed again. We call that “never spend money”.

Using the CPP Philanthropy™ strategy, their government-supplied benefits can fund the premiums on a significant life insurance policy for the benefit of favoured charities and to enhance estate values.

Estate Planing: Estate planning is putting your affairs in order so that your loved ones are taken care of if you die or are incapacitated. Estate planning goes well beyond drafting a WILL.Make sure you record your beneficiaries on your retirement and investment accounts so there's no delay in transferring the money. Estate planning includes:

- • A valid WILL

- • Naming beneficiaries

- • Setting up a trust

- • Choosing a Power Of Attorney

- • Making charitable donations

Tax Planning: ![]() Practice without knowledge is dangerous. As a professional Advisor, my ongoing learning can provide me new and important information that enhance my skills and overall knowledge.

I'm thankful to all my friends, and well-wishers for your continuous support in achieving my goal

Whether you’re a serial investor or just bought your first major investment, there’s no better feeling than saving money on your taxes. And having the right financial tools and strategies in place can make all the difference.

I am their to provide best advice on how to protect—and keep more of your hard-earned money. My tax-saving strategies to help you lower your tax bill.

Practice without knowledge is dangerous. As a professional Advisor, my ongoing learning can provide me new and important information that enhance my skills and overall knowledge.

I'm thankful to all my friends, and well-wishers for your continuous support in achieving my goal

Whether you’re a serial investor or just bought your first major investment, there’s no better feeling than saving money on your taxes. And having the right financial tools and strategies in place can make all the difference.

I am their to provide best advice on how to protect—and keep more of your hard-earned money. My tax-saving strategies to help you lower your tax bill.

Employee Benefit Plans: ![]() Employee benefits encompass a vast range of topics in the Canadian workforce. First, Employment Insurance and Canada Pension Plan premiums must be deducted from employees’ paychecks by their employer. Secondly, employers must also implement workplace insurance coverage and provide paid vacation days or vacation pay to full time staff. In addition to federally mandated employee benefits, there is an increasing number of types of employee benefit plans available to meet the needs of a diverse workforce.

The most common employee benefit plans include life insurance, health insurance, disability insurance, and retirement.

Employee benefits encompass a vast range of topics in the Canadian workforce. First, Employment Insurance and Canada Pension Plan premiums must be deducted from employees’ paychecks by their employer. Secondly, employers must also implement workplace insurance coverage and provide paid vacation days or vacation pay to full time staff. In addition to federally mandated employee benefits, there is an increasing number of types of employee benefit plans available to meet the needs of a diverse workforce.

The most common employee benefit plans include life insurance, health insurance, disability insurance, and retirement.

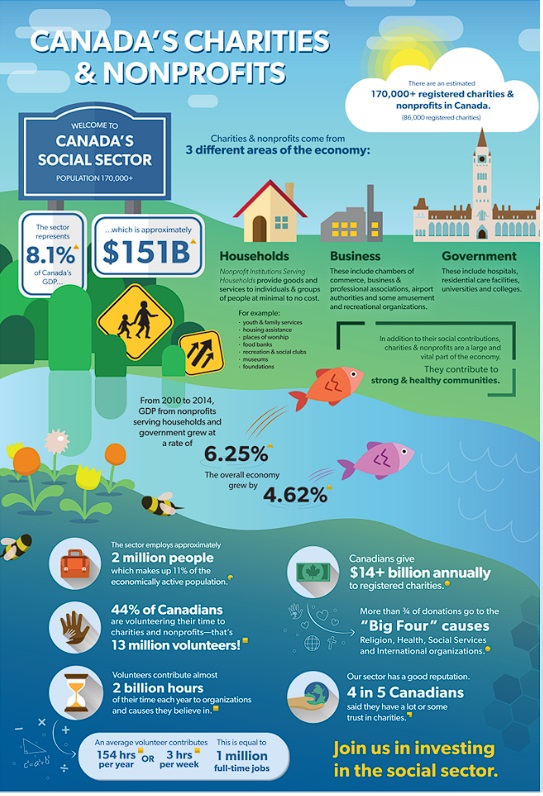

Philanthropy & Charitable Giving: ![]() Charities and non-profits are funded by various sources including earned income from the sale of products and services, individual or corporate donations, and government funding and foundation grants. Many assume that charities and nonprofits are funded mostly by government sources. This is not universally the case.

Some organizations receive no funding from any government source. For perspective, sales of goods and services account for 45.1% of total income for the core non-profit sector.

Hospitals, universities and colleges, are the exception to this rule. Almost 75% of their funding comes from government sources; 72% is from provincial governments. These institutions represent only 1% of organizations in number, but they represent about 66% of the total revenues of the entire sector. The following infographic developed by Imagine Canada (an organization that will be described later in this module) provides a helpful summary of the key statistics associated with Canada’s charitable sector.

Charities and non-profits are funded by various sources including earned income from the sale of products and services, individual or corporate donations, and government funding and foundation grants. Many assume that charities and nonprofits are funded mostly by government sources. This is not universally the case.

Some organizations receive no funding from any government source. For perspective, sales of goods and services account for 45.1% of total income for the core non-profit sector.

Hospitals, universities and colleges, are the exception to this rule. Almost 75% of their funding comes from government sources; 72% is from provincial governments. These institutions represent only 1% of organizations in number, but they represent about 66% of the total revenues of the entire sector. The following infographic developed by Imagine Canada (an organization that will be described later in this module) provides a helpful summary of the key statistics associated with Canada’s charitable sector.

Contact Me

Get In Touch With Me.

I would love to hear where you are in your journey and how we can help.

Cell: (437) 214 7224

Email: mihir@amstrategies.ca

Advisory Money Strategies Inc. 5580 Explorer Drive, Suite 502, Mississauga, ON L4W 4Y1